This model does not predict price direction.

It identifies whether the market is ready to deliver.

■ Introduction

In traditional macro trading, the U.S. Dollar Index (DXY) is often used as the primary benchmark for evaluating USD strength.

However, in intraday execution—particularly within session-based frameworks such as London and New York—DXY presents several limitations:

- It may lag real-time price delivery

- It is not always accessible or consistent across platforms

- It lacks execution-level granularity

As a result, relying solely on DXY can lead to delayed or misleading interpretations.

This research introduces a USD Proxy Model, designed as a faster, execution-grade alternative for evaluating USD strength—specifically in relation to XAUUSD.

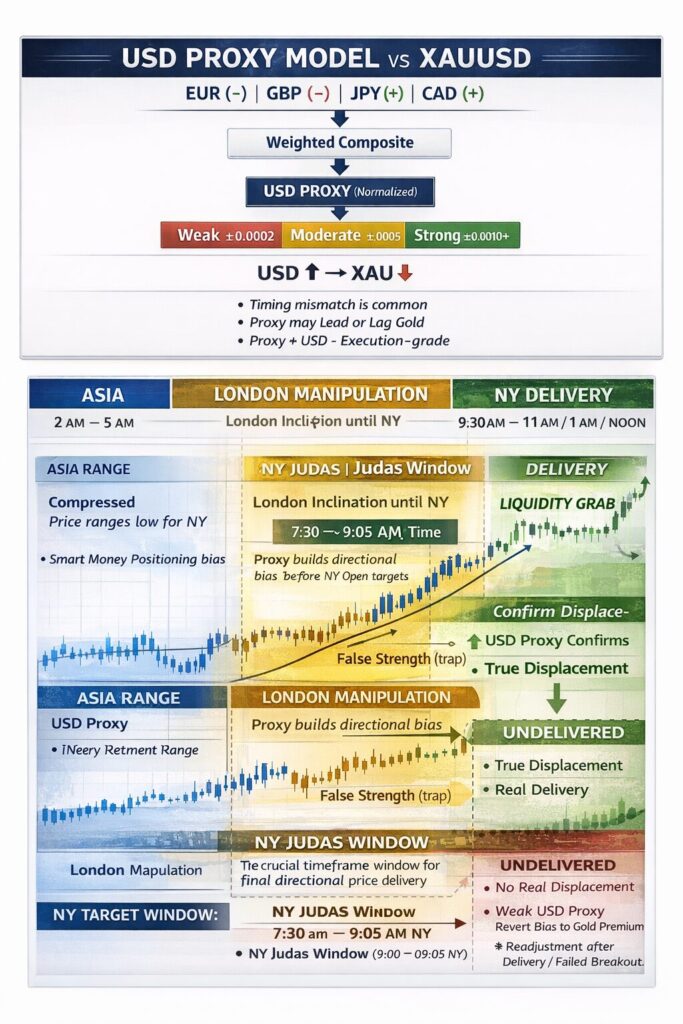

■ The Concept of a USD Proxy

The USD Proxy is constructed as a weighted composite of major currency pairs, designed to approximate real-time USD strength.

Typical components include:

- EURUSD (inverse weight)

- GBPUSD (inverse weight)

- USDJPY (direct weight)

- USDCAD (direct or adjusted weight)

Rather than attempting to replicate DXY perfectly, the objective is:

To capture intraday USD behavior in a way that is usable for execution.

■ Proxy vs DXY

- Proxy = Intraday bias (fast)

- DXY = Macro alignment (slow)

Interpretation

- Proxy leads → early positioning

- DXY confirms → true strength

- Divergence → potential trap

■ Proxy Strength Classification

To make the model actionable, the Proxy is normalized and categorized into strength levels:

- ±0.0002 → Weak

- ±0.0005 → Moderate

- ±0.0010 → Strong

- ±0.0020 → Extreme

These thresholds allow traders to quickly assess whether USD movement is:

- Noise

- Transitional

- Directional

■ Relationship with XAUUSD

Gold (XAUUSD) typically exhibits an inverse relationship with the U.S. Dollar:

- USD Strength → XAU Weakness

- USD Weakness → XAU Strength

However, the relationship is not always synchronous.

Three key behaviors are observed:

- Proxy Leading Gold

→ Indicates early positioning or institutional accumulation - Gold Leading Proxy

→ Suggests reactive movement or liquidity-driven price action - Divergence

→ Often associated with traps or incomplete delivery

Understanding when and why these occur is more important than the correlation itself.

■ Session-Based Behavior

The effectiveness of the Proxy varies significantly across sessions:

Asia Session

- Low volatility

- Proxy signals are unreliable

- Market is typically in accumulation

London Session

- Increased volatility

- Higher probability of false strength

- Proxy divergence is common

New York Session

- Directional clarity improves

- Proxy aligns with price delivery

- Most reliable for execution

This aligns with the concept of liquidity delivery cycles, where New York often finalizes directional intent.

■ Practical Interpretation (Execution Context)

While the Proxy is not a standalone system, it can be integrated into a broader framework:

- Strong Proxy + NY displacement → continuation bias

- Weak Proxy during London expansion → potential reversion

- Divergence → caution / trap scenario

The key principle is:

The Proxy provides context—not signals.

■ Limitations

- The Proxy is not identical to DXY

- Weighting schemes affect output behavior

- Lag and noise still exist

- Macroeconomic events can invalidate intraday models

This model should be treated as a supplementary analytical tool, not a predictive mechanism.

■ Conclusion

The USD Proxy Model offers a practical way to interpret dollar strength within an intraday, session-based framework.

Rather than relying on delayed or generalized indices, this approach focuses on:

- Speed

- Structure

- Execution relevance

Ultimately, the goal is not to predict the market, but to better understand:

How and when price is being delivered.

“This model is not designed to predict price. It is designed to understand whether price is ready to move.”